Americans are not saving enough for retirement, and new research co-authored by Professor Johan Walden shows one reason why: They’re misled by conspicuous consumption in their social networks.

“Our neighbors don’t put out a sign showing how much they’ve set aside for retirement, but it’s easy to see the new car sitting in their driveway,” Walden says. “The fact is, observations of someone consuming are more salient than observations of someone saving, and so we observe more of those signals, and we give them more weight in our own decision-making.”

Modeling the effect of visibility bias

A recent estimate suggests that the gap between what U.S. consumers are saving and what they’ll need to retire is almost $3.7 trillion. Some simply don’t have the income they need to set money aside. But that’s not the whole explanation.

In an article published in The Journal of Finance and co-authored with colleagues from the University of Toronto and the University of Southern California, Walden shows that “visibility bias” contributes to this chronic undersaving. Because people don’t tend to publicly share their savings habits, consumers’ social networks provide inaccurate signals about peers’ financial behavior. Consumers tend to think their peers are spending more than they are. This, in essence, makes people believe that it’s safe to consume more.

In modeling this dynamic, the researchers find that this effect feeds back on itself. As people see their neighbors and friends buy more, they may raise their rate of consumption; in turn, their neighbors see this increase and bump up their own levels of consumption, continuously squeezing savings out of the picture.

The research also shows that denser and more extensive networks are likely to intensify visibility bias. Given this, city dwellers are more likely to undersave for retirement. Growing connectedness through social media, as well as the window it gives into other people’s purchases, is also likely to exacerbate the problem, though Walden’s study did not research this specifically.

Finally, the demographics of a person’s social network could naturally reduce the strength of this bias. People who are more financially sophisticated tend to consume less as do people who are older. If someone’s social network contains more of these types of people, “then we find a dampening effect, as you’re receiving signals of low consumption from these groups,” Walden says. “But this doesn’t completely offset overconsumption among younger generations.”

More disclosure could increase savings

The effects of undersaving ripple across society, pushing people to work into older age longer than they otherwise would. People take on more debt, which, in turn, drives up interest rates. Fortunately, policy interventions may be relatively straightforward.

“The fact is, observations of someone consuming are more salient than observations of someone saving.”

One solution the researchers suggest is to reveal information about savings and consumption within social networks. Policymakers or marketers could publicize how and how much people save, thereby illuminating the unseen and reducing the influence of visibility bias. Marketing campaigns could also clarify how much people actually consume. One study from 2020 shows that giving people who overconsume information about average consumption reduced their spending by 3%.

But given people’s propensity to believe that others consume more than they do, it’s important toprovide appropriate information, Walden says. Simply publishing aggregate saving and consumption data may not be helpful, since these are already affected by visibility bias. Policymakers should take social networks and demographics into account—for example, by emphasizing consumption habits of older adults. “The more specific, the better,” Walden says.

Spring 2024|By Dean Ann Harrison| Photo: Noah Berger

Haas at the forefront

I am thrilled to share with you here our latest teaching and research advancements that are keeping Berkeley Haas the heart of what’s next

Thanks to generous donors, we are positioning Haas as the preeminent hub for behavioral economics, shaping the future of AI in healthcare, and deepening our students’ ability to accelerate the transition to a low-carbon economy with a new dual-degree option and a pioneering Climate Solutions Fund class.

This issue also celebrates the teaching of professional faculty member Stephen Etter, BS 83, MBA 89. He is transforming his longtime independent study class for athletes wanting to prepare for the financial realities of turning pro into a class that addresses the needs of current student-athletes earning money through sponsorships.

Finally, we look to Asia to see how several of our alumnae are evolving finance work there. They all share interesting insights about new opportunities for both the developed and emerging economies of the continent. Enjoy the issue!

Spring 2024|By Michael Blanding| ILLUSTRATION: ISTOCK

The key to a fulfilling relationship

In writing an effective online dating profile, the average love-seeker is likely to fill it up with appealing qualities and interests that make them special.

They paraglide, do hot yoga, and are a Libra with Scorpio rising. There’s one thing they routinely leave out, however: what they want to know about their potential partner.

Yet, that detail might be the most important thing to include, according to research by Associate Professor Juliana Schroeder.

“People want to be known, so they’re looking for partners who will know them and support them,” she says. “But because other people also want to be known, they end up writing these not-super- appealing profiles when trying to attract partners.”

Schroeder and co-author Ayelet Fishbach of the University of Chicago Booth School of Business conducted a series of experiments gauging the impact of feeling known on relationship satisfaction. They found that the degree to which someone knew another person mattered less in how they felt about the relationship compared to the degree to which they felt they were known and thus supported—regardless of how they felt about the overall quality of the relationship.

The degree to which someone knew another person mattered less in how they felt about the relationship compared to the degree to which they felt they were known and thus supported.

Their research, published in theJournal of Experimental Social Psychology, argues that this phenomenon occurs not only with romantic couples but in all manner of interpersonal relationships, including friends, neighbors, family members, work colleagues, and casual acquaintances. The one exception was parent-child relationships.

This was also apparent when they looked at online dating profiles. The researchers asked several dozen participants to write their own profiles, either emphasizing being known or getting to know the other person. More than 250 other people rated these profiles according to how much they found them appealing and would potentially want to contact them. The raters preferred profile writers who emphasized wanting to know the other person.

These findings could be instructive for someone seeking maximum appeal on a dating site, says Schroeder, the Harold Furst Chair in Management Philosophy & Values.

“What they want to be doing is saying, ‘I really care about you, and I’m going to get to know you and be there for you and listen to you and be a great partner.’”

These days, we’re bombarded with images on picture-packed news sites and social media platforms. And much of that visual content, according to new research, is reinforcing powerful gender stereotypes.

Through a series of experiments and with the help of large-language models, Assistant Professors Douglas Guilbeault and Solène Delecourt found that Google Images exhibit significantly stronger gender bias for both female- and male-typed categories than text from Google News. What’s more, while the text is slightly more focused on men than women, this bias is over four times stronger in images.

Delecourt says that most of the previous research about bias online has focused on text. “But we now have Google Images, TikTok, YouTube, Instagram—all kinds of content based on modalities besides text,” she says. “Our research suggests that the extent of bias online is much more widespread than previously shown.”

To zero in on gender bias in online images, Guilbeault, Delecourt, and colleagues designed a novel series of techniques to compare bias in images versus text and to investigate its psychological impact in both mediums.

First, the researchers pulled 3,495 social categories—which included occupations like “doctor” and “carpenter” as well as social roles like “friend” and “neighbor”—from Wordnet, a large database of related words and concepts. To calculate the gender balance within each category of images, the researchers retrieved the top hundred Google images corresponding to each category and recruited people to classify each human face by perceived gender.

Large-language models measured gender bias in online text by noting the frequency of each social category’s occurrence alongside references to gender in Google News text. The researchers’ analysis revealed that gender associations were more extreme among the images than within text. There were also far more images focused on men than women.

In another study, 450 participants searched Google for apt descriptions of occupations relating to science, technology, and the arts. One group used Google News to upload textual descriptions; another group used Google Images to upload pictures of occupations. Compared to those in the text and control conditions, the participants who worked with the images displayed much stronger gender bias associating women with arts and men with science (a bias linked to systemic inequalities in academia and industry)—even three days later.

“This isn’t only about the frequency of gender bias online,” says Guilbeault, the paper’s lead author. “There’s something very sticky, very potent about images’ representation of people that text just doesn’t have.”

E-waste is the world’s fastest-growing solid waste stream, and companies are struggling with a deluge of waste produced by their manufacturing processes and products. Some have been illegally exporting their e-waste—which may contain hazardous substances that need special treatment—or illegally dumping it closer to home.

In 2021, for example, Amazon was caught trashing some 130,000 unsold or returned items in a U.K. warehouse—including laptops, smart TVs, and other electronic devices—in one week. The company acted in line with financial incentives: Destroying these goods was cheaper than storing, repurposing, or recycling them.

These clashing incentives are causing waste processing systems to fall far short of best practices, according to research co-authored by Assistant Professor Sytske Wijnsma. The paper offers recommendations to help regulators improve ineffective laws.

Simulating waste streams

It’s estimated that 75% of e-waste globally is exported, typically from the EU or U.S. to developing countries, where disposal is less regulated. Only slightly over a third of the EU’s e-waste is properly handled.

Wijnsma and her colleagues constructed a model to simulate where waste typically leaks from the waste disposal chain, incorporating two key actors: a manufacturer producing waste and a treatment operator responsible for treating waste within a country.

Waste producers either generate high-quality waste—with resale value from its component parts—or low-quality waste, which is more hazardous and less valuable post-treatment.

Clashing incentives are causing waste processing systems to fall far short of best practices.

Typically, a treatment operator sets a price to manage a batch of waste without knowing whether it’s high or low quality.

The waste producer decides whether to contract with the treatment operator or to export it—legally or illegally, in which case it leaks from the system, often landing in developing countries where environmental regulations are spotty. Many countries prohibit low-quality waste export, while higher-quality waste export often remains legal.

Even if a producer contracts a local operator, proper treatment is not guaranteed. The operator might still opt to dump it illegally rather than disassemble it, immobilize hazardous substances, and recycle it for revenue. “If an operator thinks there’s a very high probability of only getting bad waste, then they might be more inclined to dump it.”

Addressing system breakdowns

The model highlights two key reasons the e-waste treatment chain breaks down. First, there are few if any consequences for waste producers when their contracted treatment operators violate regulations.

Second, current export policy focuses solely on prohibiting the export of low-quality waste. As such, waste with low post-treatment value is increasingly retained locally, causing treatment operators to raise the price of treatment. That, in turn, drives the more valuable waste to be sent abroad where treatment costs are lower. Consequently, local operators are left with primarily low-quality, unprofitable waste and have more incentive to dump it.

When it comes to policymaking, Wijnsma and her colleagues say that regulations that treat high- and low-quality waste dramatically differently create perverse incentives and are likely to backfire. The researchers also recommend holding waste producers partially responsible when their downstream waste is disposed of improperly.

Chances are, that gym membership you signed up for with the best of intentions on January 1 might already be underused. Next time, consider signing up with a friend.

New research by Asst. Prof. Rachel Gershon suggests that pursuing our goals with friends may make them more attainable. Gershon and colleagues from Washington University and the University of Pennsylvania specifically looked at gym visits and found that going with a friend—even with the hurdles of coordinating two schedules—increased visits by 35%.

In the experiment, participants were paired up with a friend and given either one dollar every time they went to the gym, regardless of their friend’s activity, or one dollar if the two of them went together.

The researchers concluded that two benefits eclipsed the logistical costs of coordinating with a friend. First, people enjoyed their visits more when the event was social, making future visits more likely. Second, they felt a greater sense of accountability.

“Our study identifies two types of accountability,” Gershon says. “People feel responsible to their friends, as they wanted them to get the reward, but they may also have reputational concerns that their friends would think less of them if they didn’t follow through.”

Beyond this experiment, the findings illustrate how building a social dimension into desired behaviors can promote follow-through. Companies wanting to increase employee engagement with skills training, for instance, could try a joint-incentive program to boost participation.

Catalyzing American entrepreneurship to look like America

Even though professional faculty member Maura O’Neill, BCEMBA 04, started her first company 40 years ago, the hurdles she faced as a female entrepreneur are largely the same ones currently faced by her students who are women and/or students of color. “These Berkeley students are super smart, have great ideas with grit oozing out of their DNA,” says O’Neill. What are we missing as a community and as a nation, she wondered, by leaving this talent on the sidelines, particularly when both the problems and the opportunities are huge?

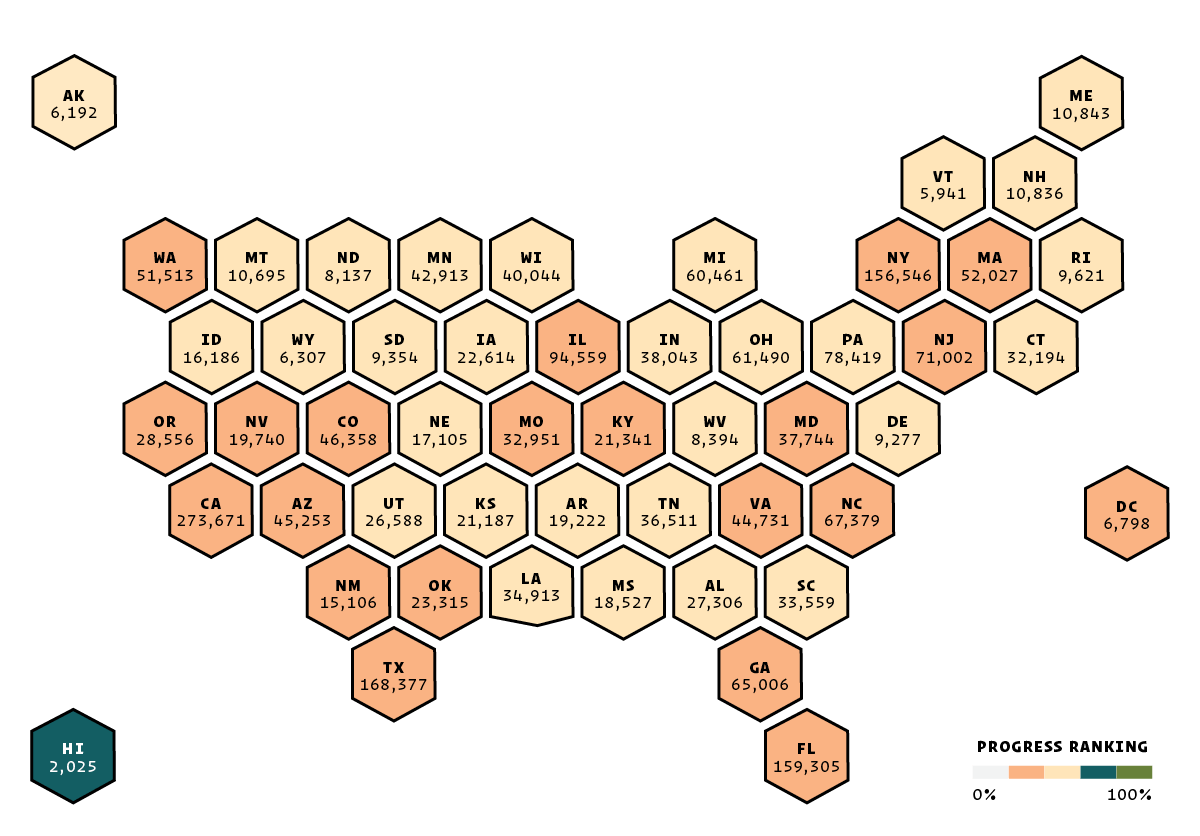

O’Neill analyzed big data sets and found that if American business ownership reflected the race, ethnicity, and gender of the nation’s population, the country could have 2.4 million more businesses, 20 million more jobs, and a $4 trillion increase in annual GDP. At the state level, those whose business ownership more closely reflects their population have 2.5 times higher GDP than states lagging further behind. “Everyone wins when this happens,” O’Neill says.

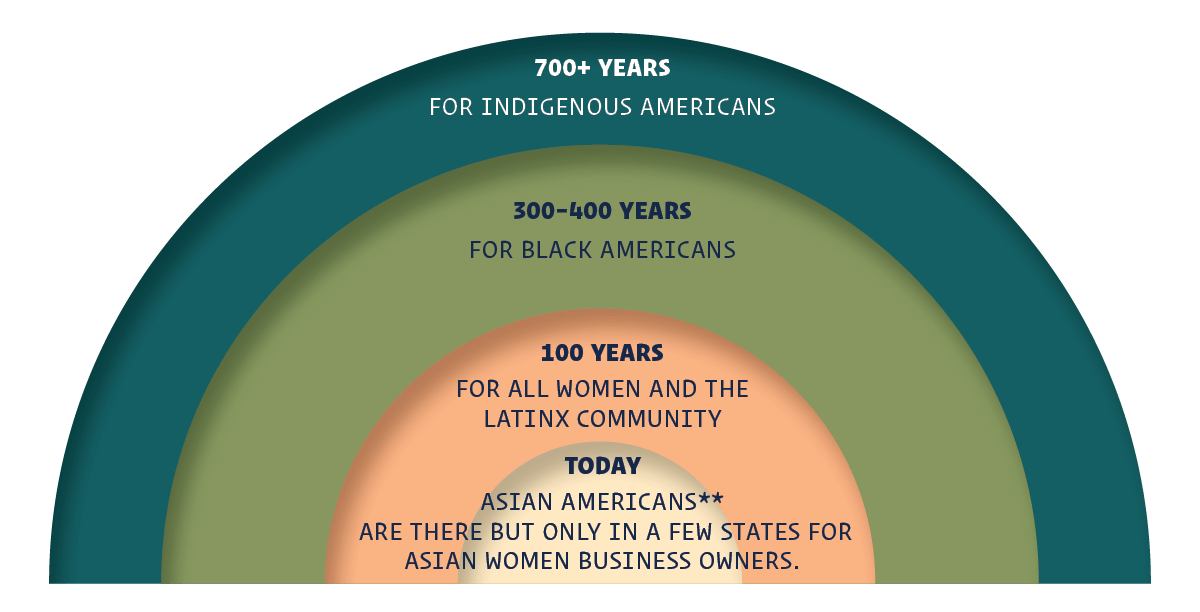

At current rates, it will take over 700 years for American entrepreneurship to look like America. But O’Neill launched The Decade Project to accelerate the path to parity in 10 years. “If we can put a man on the moon in a decade and bring him back safely without first knowing the technology,” she says, “we can do this.”

TDP’s research shows that four areas are key to success: role models, financial capital, knowledge, and connections. In addition to mobilizing a national ecosystem of partners in each of the areas, TDP is identifying ways to leverage the flood of federal and private investment dollars (estimated to be $8 trillion) associated with the transition to a sustainable economy to seize this opportunity and catalyze local leaders across the nation.

What’s in it for Your State?

The Decade Project data indicates that if American business ownership reflected the local population, the country could have over 2 million more employer firms. How many would your state gain?

How Long to Reach Equality?

At current rates, if nothing changes, it will take over 700 years for American business ownership to look like America.*

*Trends based on 2019 Census Data.

**As a whole, Asian Americans are at parity, but it is not true for every Asian subgroup.

Spring 2024|By Gail Allyn Short| PHOTO: NICK ONKEN

Growing up in New York City, Jesse Brackenbury loved visiting the parks nestled between the city’s skyscrapers.

“I had urban parks in my blood. I grew up taking gym classes in Central Park, and I’ve always been interested in environmental issues,” says Brackenbury, who ended up working for the city’s Department of Parks & Recreation after college.

That experience eventually landed him an executive director role at Boston’s Rose Kennedy Greenway Conservancy. The Greenway is an outgrowth of the Central Artery Tunnel Project, known as the “Big Dig,” which replaced an elevated highway with a tunnel system.

“People didn’t like the park when it opened,” Brackenbury says. “The Big Dig was controversial, expensive, and it took a long time.”

To boost its image, Brackenbury and his team ramped up the park’s offerings by adding 450 free events annually, including fitness classes, food trucks, rotating art installations, and a carousel.

Consequently, The Boston Globe, which once called the park “The Empty Way,” redubbed it “The People’s Park.”

In 2021, Brackenbury returned to New York City and is now president and CEO of the Statue of Liberty–Ellis Island Foundation. He’s leading a multimillion-dollar fundraising campaign to reimagine the National Museum of Immigration. It will include new exhibits and interactive media to tell the stories of the 12 million immigrants who came through Ellis Island and the broader, more inclusive history of American immigration.

“I thought there weren’t many park jobs better than the one I had in Boston,” Brackenbury says. “Joining the Statue of Liberty–Ellis Island Foundation and working on these monuments proved otherwise.”

Spring 2024|By Andrew Faught| PHOTO: SILVIA V. GUEVARA

Tawainese American Filmmaker Devin Tau developed a passion for movies while working at his parents’ video rental store in Whittier, Calif. When it came time to choose a career, however, it wasn’t an option. Still, Tau bucked convention.

“In my Asian family, there are three acceptable professions: doctor, lawyer, engineer,” he says. “My brothers became engineers; I broke the mold by doing business at Berkeley.”

Tau went on to work a decade in corporate finance, then as an apparel buyer for Gap Inc. But putting stories to celluloid was too strong a pull.

“When I turned 40, I had a midlife crisis, so I went to film school and started my own production company,” he says. “I never thought that I would be a filmmaker, mostly because it was culturally never possible.”

To date, Tau has three feature-length films to his credit: the thriller Half Sisters (2023); Who’s On Top?, the story of four LGBTQ+ athletes who climb Oregon’s Mount Hood (2021); and The Road Home (2022), chronicling six formerly incarcerated adults and their challenges to relocate while on community supervision.

Tau, who is gay, says he is driven to spotlight stories that haven’t been told before. “I’m a huge advocate for the underdog.”

Tau says there are similarities between business and filmmaking, beyond raising funds to bring a project to fruition: “If you’re creative, you have a million ideas, similar to an entrepreneur. It’s always challenging to get people to believe in your ideas if you’re not proven or you haven’t come to market with your product.”

After Jenny Zhang and her husband moved from the Bay Area to Hong Kong, it’s not surprising she eventually ended up in the real estate sector.

“There are three types of jobs in Hong Kong,” Zhang quips. “Finance, real estate, and financing real estate.”

She started out as a Deloitte M&A manager, analyzing deals totaling more than $12 billion. The job, she says, trained her to find patterns to quickly understand everything from animal vaccines to semiconductors. Zhang later launched a knowledge-sharing program to help colleagues become adept advisers across industries and markets in the shortest amount of time.

The work was exciting, Zhang says, but sustainability and climate change—topics that she explored at Haas—interested her more.

“At Haas, I was surrounded by people who felt passionate about social and environmental issues and who believed that we had the privilege and obligation to do something about them,” she says.

Zhang left Deloitte and was one of the first hires at climate-tech startup Carbonbase, working with energy and real estate companies to track their carbon emissions and to purchase carbon offsets. Yet, she wanted to do more.

In 2022, she joined the Urban Land Institute where she’s building a network of developers and investors, researching the ROI of sustainable buildings, and facilitating workshops to redesign industry practices.

Looking back, Zhang says her career path taught her that anyone can have an impactful career, no matter their role.

“My first boss at Macy’s had a quote up in his office that always stuck with me: ‘Bloom where you are planted,’” she says.

Spring 2024|By Katie Gilbert| Photos by Gareth Brown

Haas alumnae help evolve finance in Asia.

Christina MA, MBA 01 (shown at top), found her way into finance serendipitously. As an undergrad at Georgetown University, she had planned on becoming a diplomat but changed her mind before graduation. All she knew when she earned her diploma was that she wanted an international career in a dynamic city bursting with opportunity. Given her language skills, Hong Kong seemed a good bet. This was the mid-1990s, and China was in a stage of dizzying economic growth as it opened itself to capitalism and foreign investment.

After three months of networking, she landed a role as a proprietary equity trader at an Asian bank, a career she’d never considered largely because it was such a male-dominated field. “I had visions of Gordon Gekko from the movie Wall Street, of big guys in suspenders and slicked-back hair,” she recalls.

Indeed, as a woman, Ma was in the extreme minority on the trading desk. For some long periods over the course of her career, she was one of only a handful of women on the trading floor and in an even greater minority as a senior female trading manager globally. While the finance industry has made strides toward gender parity since the mid-90s, it remains male-dominated. According to a 2022 report from Deloitte, 19% of C-suite roles within the world’s financial services institutions belong to women—but just 14% in Asia.

Like Ma, the Haas alumnae featured here are impacting their respective niches of Asian finance. They represent both seasoned executives and up-and-comers, speaking to how the Asian finance industry has evolved and what’s on the horizon from their respective perches. Whether it’s helping to bring ESG (environmental, social, and governance) to prominence, establishing a burgeoning venture-capital market, or pushing for gender parity, all of these women are finding ways to encourage the many transformations underway in Asian finance to redound to inclusion, sustainability, and equity.

Shifting culture

For her part, Ma resolved that structural gender disparities wouldn’t hold her back. “I try to spend my energy and time thinking about what I can change, instead of fretting about what I am not,” she says.

That outlook has led to great career success and satisfaction. After three years working as a proprietary trader and junior portfolio manager at a local fund, she left to get her MBA at Haas. Upon graduation, she returned to Hong Kong and spent over two decades climbing the ranks at Goldman Sachs, first as a trader then becoming a partner and ultimately heading up Goldman’s greater China equities business. Since then, Ma has moved to HSBC, where she’s now the head of global banking, Asia-Pacific, overseeing a team of more than 500 bankers covering some of the largest corporate and institutional clients in the world.

As she’s traced this trajectory, Ma has strived to make finance more inclusive for both women and local talent. This has meant raising issues with her male colleagues they hadn’t come across before. When Ma was pregnant, for example, she had to work closely with her manager to develop her maternity leave plan—a first, since they had never had a senior trader go off on maternity leave.

“I hope that I have shown other women and men that you can succeed while being different from others and that the diversity of thought and style is valued and a good commercial decision.”

—Christina Ma, MBA 01

Fortunately, some key aspects of the culture around women at work have shifted since Ma was a young parent. The Chinese government has prioritized gender equality within its social development policies, and women there are moving closer to greater flexibility in their work hours, paid mental health leave, and longer maternity leaves.

Some economists argue that, across Asia more broadly, taking these types of steps to embrace women in the workforce will be crucial as the region’s population ages. A 2018 report from the McKinsey Global Institute estimates that improving women’s equality in the region could boost collective annual GDP by 12%.

Ma has been heartened by the finance industry’s increasing focus on diversity and inclusion initiatives, especially at the junior level, where incoming grad classes are often half women. But she acknowledges that diversity within finance’s senior leadership hasn’t evolved enough.

“I think there’s a realization that this is a much longer road,” Ma says.

Still, she believes that her journey and the efforts of others like her make an impact in important ways—one of them being the ripple effect of representation. “I hope that I have shown other women and men that you can succeed while being different from others and that the diversity of thought and style is valued and a good commercial decision,” Ma says.

Kin-Fun Lee, MFE 05, works at Julius Baer as head of strategy and business operations for the Markets & Wealth Management Solutions unit covering Asia.

Establishing the forefront

Kin-Fun Lee’s two-decade career in finance has afforded her a front-row seat to some of the most significant changes that have rippled through the industry in recent memory. In 2008, when the global financial crisis hastened a suite of regulatory changes across the region and world, Lee, MFE 05, was an executive director at J.P. Morgan in Hong Kong, overseeing business management and development for Asian equity derivatives and the prime brokerage businesses. During this time, she says, she was active in helping the firm weather a crisis unlike any seen in a generation. At the same time, she helped it contend with how new regulations—like the Dodd-Frank Act in the U.S. and what would become the Markets in Financial Instruments Directive (MiFID) in Europe—were changing the business.

As the dust settled, Lee felt pulled to help usher along some of the changes that these new regulations had seeded. “The main objective of the reforms post-crisis was to protect the end investor,” Lee says. “That got me started looking into a new area: I wondered how I could get closer to those end investors to see the real need and to provide solutions that really help them.”

“We’re seeing more sophisticated investors in some regions. They have a greater need for more complex, innovative, and bespoke products.”

—Kin-Fun Lee, MFE 05

She accepted an opportunity to do just that in 2013, decamping from her investment bank position for a job with the global wealth manager Julius Baer. As head of strategy and business operations for the Markets & Wealth Management Solutions unit covering Asia, Lee has been instrumental in developing and deploying new investment products. Her role involves assessing client demand, ensuring regulatory compliance, and aligning products with the bank’s infrastructure. For example, she and her team have been supporting the integration of new asset classes (e.g. digital assets) into traditional formats of financial instruments, like exchange-traded funds and structured products.

Anticipating what investors will need keeps Lee, her firm, and the industry on the cutting edge—an increasingly complex endeavor, she acknowledges, as some of the fast-developing Asian economies attract growing investor interest.

“We’re seeing more sophisticated investors in some regions,” Lee says. “They have a greater need for more complex, innovative, and bespoke products while at the same time fully complying with the regulators’ requirements.”

Lee predicts “continuous growth” in investor interest in Asia as a whole. As that interest continues to pour in, she sees another shift happening in terms of the investment products investors will need: “In the last generation, investors in Asia were more focused on wealth creation,” Lee says. “But now, it’s more to the stage of wealth preservation—and passing wealth along to the next generation.” Lee plans to play a central role in crafting the investment products they need to do just that.

Encouraging ESG

Anni Zhang, too, is out to update some of the ways the finance industry has done business in the past. Her focus, though, is on pushing the industry to factor in previously ignored environmental and social risks—and opportunities.

“I’ve been able to play a huge role by educating people. It can be uncomfortable for traditionally trained finance professionals to include ESG into their customary analytical framework.”

—Anni Zhang, BS 14

Zhang, BS 14, is an ESG associate for Asia-Pacific-focused private credit firm ADM Capital in Hong Kong—and, she explains, is “basically responsible for everything ESG-related day-to-day.”

Across the entire investment process—from deal sourcing to advising the investment team on the relevance of ESG factors to financial performance—Zhang is helping to ensure that environmental and social factors are taken into account. It also means creating ESG action plans for portfolio companies (which are all small- and medium-sized enterprises in Asia) and working those plans into their loan covenants. And it involves monitoring and reporting on borrowers’ ESG performance.

Anni Zhang, BS 14, is an ESG associate for Asia-Pacific-focused private credit firm ADM Capital.

ADM’s founders were pro-ESG at the outset, Zhang says, and in her two years with the firm (in addition to two years with its foundation arm) she’s pounced on the opportunity to push its ESG practices to the forefront of the industry.

“I’ve been able to play a huge role by educating people,” she says. “It can be uncomfortable for traditionally trained finance professionals to include ESG into their customary analytical framework. Over time, though, I’ve seen a change in mindset with our deal teams and with the broader industry. ESG is now a key competitive advantage of ADM.”

Zhang doubled-majored at Berkeley in business and conservation and resource studies, a dual focus that she says has been instrumental in helping her to reconcile the perspectives of both finance teams and sustainability experts. In Asia, bridging these perspectives will prove increasingly critical, she says. Not only are regulations and disclosure requirements pertaining to sustainability developing quickly—but the health of the region (not to mention the planet) may depend on it.

“I see a bigger opportunity for ESG here in Asia because there are so many underdeveloped cities and economies, so there’s a lot more opportunity to do good and contribute to their development in a way that’s sustainable,” Zhang says. “There’s also incredible nature and biodiversity here. So much is at stake.”

Advancing developing economies

In the most developed parts of Asia, many of the movers and shakers within the finance industry are rooted in—and most familiar with—the region’s major financial hubs, like Hong Kong, Tokyo, and Singapore. Not so for Tab Boonthaveepat, MFE 11, an executive director and trader at Goldman Sachs in Hong Kong covering Asian emerging markets—and she considers this distinction one of her great assets.

Boonthaveepat traces her roots to Bangkok, where she grew up and began her career (after earning her MFE at Haas) as a quantitative portfolio manager at hedge fund Phatra Securities.

Tab Boonthaveepat, MFE 11, is an executive director and trader at Goldman Sachs in Hong Kong covering Asian emerging markets.

The many economies across Asia represent a vast diversity in their stages of development, Boonthaveepat points out. Beyond the major financial hubs, other countries, like Vietnam and Indonesia, are emerging, and the rapidly growing Indian economy is somewhere in between. Thanks in part to her background and work experience in Thailand, Boonthaveepat is deeply invested in understanding (and explaining to others) how each of these markets presents investors with its own constraints—and opportunities.

“I always want to make sure that I’m helping these small markets have a chance in the global arena.”

—Tab Boonthaveepat, MFE 11

“Emerging markets in Asia are changing,” Boonthaveepat says. “And I think especially since the pandemic, we’re seeing more interest from global investors in India and also in some of the small Southeast Asian markets.”

She’s committed to connecting this growing interest from global investors to the markets that could benefit from their capital. “I always want to make sure that I’m helping these small markets have a chance in the global arena,” Boonthaveepat says. “That’s something I’m very proud of.”

Tracking what’s next

Aparna Chaganty, MBA 23, is also interested in bringing Asia’s investment opportunities to the world, and she’s working to do so within India’s burgeoning venture capital industry. “VC, as you see it today, was simply not prevalent in India 25–30 years ago,” says Chaganty, an investor based at the Bangalore office of global VC firm Bessemer Venture Partners. “There were not enough startups to create an ecosystem for multiple large VCs to come and play here.”

“It’s an incredibly dynamic market we’re in right now, and I want to leverage my Silicon Valley experience to help Indian startups compete and win on a global stage.”

—Aparna Chaganty, MBA 23

Chaganty’s work involves meeting founders who are launching India-born startups angling for a global audience. Thanks to the rate of Asia’s—and especially India’s—economic growth, she says the opportunities to be found in the region today are unique. Pair Asia’s growth with Chaganty’s industry focus on software—which is also evolving dramatically due to the development of AI—and you get “a very special point in time to be part of this industry,” Chaganty says.

Aparna Chaganty, MBA 23, works as an investor based at the Bangalore office of global VC firm Bessemer Venture Partners. Photo: Harshith Dambekodi.

“With the advent of AI, the market is on the precipice of a transformation,” she says. For one thing, small, lean startups are able to command more scale and revenue because of the power of their underlying software. At the same time, their business models face the challenge of having to find ways to continue driving value, even as the underlying software rapidly evolves. “It’s an incredibly dynamic market we’re in right now, and I want to leverage my Silicon Valley experience to help Indian startups compete and win on a global stage.”

Chaganty extends an invitation to her fellow Haas alumnae to join her on the exciting ride. Like many other parts of finance, the VC industry is still male-dominated, and Chaganty believes it could benefit from the perspectives of more women.

What’s more, she believes such a dynamic market is likely to beget a dynamic career. “Riding the wave of the special moment we’re in here can also mean a lot of learning and personal growth as well,” Chaganty says. “That’s the bet I made.”

Chris Hulls has given millions of parents worldwide peace of mind. He’s the co-founder and CEO of San Francisco-based Life360, a family-focused location-sharing app. It now also allows users to connect and track pets and objects as well as offers emergency assistance, identity protection, and more. Hulls got the idea for Life360 after Hurricane Katrina in 2005 and mapped out his business plan in an entrepreneurship class at Haas. As a student, his idea won $275,000 in a Google software challenge. Along the way, he’s leaned on Haas connections to grow the company into the largest location-sharing app, with over 60 million active users worldwide. Here’s a look at how he did it.

2008

Life360 launches to keep families safe. In its first three years, 25 million users sign up. Collectively, they share more than 150 billion location points—or 2,500 locations every second.

2012

The company wins a prestigious Webby Award and launches a geo-fencing feature, called “Places,” that allows users to receive alerts for specific locations. Angel investor Mark Goines, MBA 76, introduces Hulls to Itamar Novick, MBA 12, who joins the company as a stakeholder and spends nearly a decade there, mostly as chief business officer.

2013

The new “Circles” feature allows for private connections with friends, babysitters, dogwalkers, and other non-family members.

Image: iStock.

2014

Despite only being available in English, Life360 experiences 260% growth internationally and responds by launching in eight languages.

2019

Life360 goes public on the Australian Stock Exchange (ASX) under the ticker “360.”

2020

Responding to young users’ complaints about overbearing parents infringing on their privacy, Life360 develops “Bubbles,” which give teens the ability to show their general (but not exact) location.

2021

Life360acquires Tile, a consumer electronics company known for its tracking devices, for $205 million. Families in 195 countries now use the app.

2023

The company cuts 14% of its staff and achieves adjusted profitability in Q1, faster than expected. Market value exceeds $1.4 billion, and growth continues as an in-house survey shows that Gen-Z embraces location sharing for its sense of safety.

Spring 2024|By Laura Counts, Amy Marcott, Kim Girard, Dylan Walsh, Mickey Butts | Illustrations: Brian Stauffer

Berkeley Haas’ commitment to educating future-oriented leaders demands a constant evolution of our teaching and research. Here, we highlight two new research centers whose work will keep Haas at the forefront of behavioral economics and drive positive healthcare innovations. As well, we feature a new climate solutions dual-degree program and a new fund-based class to prepare students to lead the transition to a more sustainable future.

Leading the Next Wave of Behavioral Economics

By Laura Counts & Mickey Butts

Ever since future Nobel laureates George Akerlof and Daniel Kahneman created a 1987 UC Berkeley course that broke the barrier between psychology and economics, the university has led the way in bringing these disciplines together into the field of behavioral economics.

In the ensuing years, psychology-based behavioral economics has explored the predictable foibles in our thinking, such as decision-making biases, fears of losing out, lack of self-control, and overconfidence. A classic example is Kahneman’s pioneering work with Amos Tversky on loss aversion, which showed that people are willing to take greater risks to avoid a loss than to secure a gain.

Now Haas is poised to lead the next wave, pushing the field beyond psychology and gleaning insights from disciplines as diverse as neuroscience, biology, and medicine with the launch last fall of the Robert G. and Sue Douthit O’Donnell Center for Behavioral Economics.

“Humans are living, breathing organisms affected by their unique life paths,” says Professor Ulrike Malmendier, the O’Donnell Center’s founding faculty director. “We have minds and bodies, and an economic science that describes human behavior needs to account for both.”

Thanks to a philanthropic investment of almost $17 million by Bob O’Donnell, BS 65, MBA 66, and his wife, Sue O’Donnell, the center will advance the next generation of research, extend learning opportunities to students, and position Haas as the preeminent hub for the field. Malmendier aims to bring in leading researchers from a wide range of disciplines for collaboration, conferences, and bootcamps—beyond what has been considered part of the field. The center will also provide fellowships to PhD students and postdoctoral scholars and will host the prestigious Behavioral Economics Annual Meeting (BEAM), co-founded by Malmendier, every three years.

Bob, BS 65, MBA 66, and Sue O’Donnell look forward to the interdisciplinary opportunities the new O’Donnell Center for Behavioral Economics will create for researchers and students alike. “UC Berkeley is dedicated to integrating business education with other disciplines on campus, which is essential in this area,” Bob says. “It should have a center devoted to continuing this work.”

Students will benefit from a curriculum enriched by the foremost thinkers in the field. In early April, for example, the O’Donnell Center co-sponsored a fireside chat with economist and Nobel Laureate Richard Thaler and New York Times writer David Leonhardt. Malmendier has also initiated a weekly reading group with faculty, PhD students, and post-docs to discuss the latest behavioral economics research. Such discussions will deepen the knowledge faculty bring to the classroom. And because of the interdisciplinary nature of the O’Donnell Center, the teaching of behavioral economics and finance will expand to students campuswide.

Breaking new ground

Malmendier’s goal is to open a new frontier in research that will help business leaders and policy makers. “We went from neoclassical economics that considered humans to be perfectly rational to behavioral economics that brought in social psychology,” explains Malmendier, the Cora Jane Flood Professor of Finance.

For example, after Nobelist Thaler and Cass Sunstein developed the concept of the “nudge”—interventions that spur people to act in their own self-interest, such as enrolling them in a retirement savings plan by default—hundreds of “nudge units” were established in governmental and private-sector organizations around the world. Just last spring, a report from the National Academies of Sciences, Engineering, and Medicine called for increased collaboration between behavioral economists and policymakers in part to encourage people to make better decisions.

“Now we want to move the needle further, bringing together the best minds for rigorous research on human behavior from the sciences more broadly, including neuroscience, cognitive science, biology, medicine, epidemiology, and genetics,” Malmendier says.

Pioneering collaborations

For her part, Malmendier will expand her groundbreaking work on “experience effects,” which earned her a Fischer Black Prize in 2013 for the top economist under the age of 40—the only woman to ever win the prize—and a Guggenheim Fellowship in 2017. She has studied how stressful experiences with recessions, layoffs, inflation, housing bubbles, and political repression make consumer and investor behavior more cautious and risk averse for years afterward. She’s also explored how stress can affect our health, careers, education, and other aspects of life in dramatic ways.

Now, she aims to further that work by collaborating with neuroscientists, neuropsychiatrists, biologists, medical researchers, and epidemiologists who have studied stress and trauma—insights that could more precisely demonstrate how past experiences shape our actions, such as completing an education, choosing an occupation, and deciding to have a family, today and across generations.

“As we walk through life, our outlook on the world changes, especially if we suffer trauma,” she says. “Neuroscience says our brain gets rewired. There may be a long-term impact of stress on our longevity, on our aging, and on our health.”

In addition to Malmendier, the center will include a host of affiliated researchers from Haas and Berkeley Economics and elsewhere across the university. They include center co-founder Stefano DellaVigna, professor of economics and business; Haas professors Ricardo Perez-Truglia, Ned Augenblick, Don Moore, and Gautam Rao, PhD 14 (who recently joined Haas from Harvard University); as well as Dmitry Taubinsky of Berkeley Economics, and others.

“We want to move the needle further, bringing together the best minds for rigorous research on human behavior from the sciences more broadly, including neuroscience, cognitive science, biology, medicine, epidemiology, and genetics.”

—Prof. Ulrike Malmendier

Shaping transformative leaders

Founding donor Bob O’Donnell says he was inspired by the interdisciplinary promise of behavioral economics at Haas. “UC Berkeley is dedicated to integrating business education with other disciplines on campus, which is essential in this area,” he says. “It should have a center devoted to continuing this work.”

O’Donnell, a retired portfolio manager for a large mutual fund group, often applied insights from behavioral economics during his career. “When combined with existing financial theory, I believe that its insights enhanced results for my clients,” he says.

Yet, during the 17 years O’Donnell taught an investment class in the Berkeley Haas MBA program, he says he sometimes encountered skepticism when introducing ideas from the field. “Indeed, one student asked, ‘Isn’t all this kind of woo-woo?’” he says. “Several years later, that student told me how perspectives from behavioral economics had helped her career in finance.”

O’Donnell envisions his endowed gift as one that will not only define the future of behavioral economics but shape truly transformative leaders. Founding the center, he says, is a start but more investment is needed to enhance curricular offerings and expand the groundbreaking research that will be the hallmark of the O’Donnell Center.

Malmendier is passionate about the potential of behavioral economics to help leaders create better solutions to the most complex and urgent problems of our time, like battling inflation. “If leaders keep in mind people’s emotions, their personal histories, and their psychologies,” Malmendier says, “they can engineer ways to make things more predictable and give people more control over events to help them live better lives. That is our ultimate goal.”

Harnessing AI to Transform Healthcare Outcomes

By Amy Marcott and Laura Counts

The U.S. spends almost 20% of its gross domestic product on healthcare—more than any other high-income country. Yet we see a low return on that investment: Americans have poor outcomes across numerous dimensions, including life expectancy.

A big factor in these poor outcomes is a healthcare system that resists easy remedies, says Haas Professor Jonathan Kolstad. Promising innovations and technologies are often dead on arrival due to lack of understanding of the incentives at play.

“There’s a big gap between the kinds of AI and machine learning tools that are being built for healthcare and the realities of the healthcare delivery system, including the complex incentives, how the system functions, who would buy the product, and who would use it,” he says. “Conversely, the healthcare system is behind in terms of the technology, the systems, and the adoption of new AI tools. Right now, there’s a unique opportunity to play massive catch-up.”

The new Center for Healthcare Marketplace Innovation (CHMI), a joint endeavor between Haas and Berkeley’s new College of Computing, Data Science, and Society, aims to bridge that gap with solutions that join AI and data science with behavioral economics and an understanding of the realities of the healthcare system and the vagaries of human behavior.

Launched this spring with a gift from an anonymous donor, the CHMI combines technology development and academic research, giving researchers and partners access to a massive database of healthcare data. In fact, CHMI is believed to be the first applied research center of its kind to merge data, behavioral economics, and artificial intelligence with a focus on technology incubation.

Applied behavioral economics

Previous approaches to healthcare innovation are often too simplistic, Kolstad says, while other technologies have simply aimed to replace doctors. “These are some of the smartest and most highly trained humans making lots of different decisions under complex situations—which machines simply cannot do,” he says. “It’s the interaction of technology and human decision-making where AI is going to meet the market in healthcare.”

Take, for example, helping a radiologist better identify cancer. To do so successfully, Kolstad says, requires understanding the realities of how radiologists work, what they try to do, when cancer is spotted, who’s being screened, what data are available with the right pictures, and even how they’re paid. “All of those layers are critical,” he says.

Kolstad is building a database that he hopes will be one of the largest multimodal healthcare data platforms in the world. This rich data will include health insurance claims as well as medical records, images, electrocardiogram waveforms, and other granular information all linked to longitudinal health outcomes. The platform will be available for both research and R&D. “We want to structure it so that you can use the data to learn and create new insights but also create new solutions that really meet patients where they are,” Kolstad says.

“It’s the interaction of technology and human decision-making where AI is going to meet the market in healthcare.”

—Prof. Jonathan Kolstad

In addition to this novel data platform, CHMI will also offer academic and industry partnerships to facilitate the development of new AI and technology solutions grounded in real-world problems; the incubation of new companies; and academic research on AI, behavioral economics, and economic incentives. The interdisciplinary center will work with researchers throughout UC Berkeley and at UCSF.

The importance of incentives

What’s key to success, Kolstad says, is working within the constraints of a complex, market-driven healthcare system bolstered by governmental incentives. “At the end of the day, you have to understand the incentives in order to create solutions that are going to get to scale and change things,” he says. “We’re facilitating what we think will make that system more effective, more productive, and more efficient, which will lead to better health at a lower cost.” Kolstad himself has done this with the launch of a new company, Healthpilot, to help improve Medicare (see sidebar, “Haas Research Fuels Company Benefiting Medicare Patients”).

“My strong hope for CHMI is that there will be novel technologies that will be positioned to create new startups, nonprofits, or open-source solutions,” says Kolstad, the Henry J. Kaiser Chair. He’s forming relationships with venture funds, big insurers, and government agencies keen to see CHMI innovations—executives who can collapse the time it typically takes to run a pilot and scale. “We’re here to actually change things,” Kolstad says.

Doubling Down on Sustainability

By Kim Girard and Laura Counts

Since Dean Ann Harrison assumed leadership of Haas five years ago, she has made sustainability a strategic priority for the school, working to ensure that students are trained to view leadership challenges with a sustainability lens. Undergrads can now minor in sustainability, MBA core courses are being revamped to incorporate thinking about climate change and other sustainability challenges, and Haas launched the Michaels Graduate Certificate in Sustainable Business, to name just a few offerings.

Now, MBA students wishing to deepen their training in the field have two new opportunities available to them: a dual-degree option and a pioneering Climate Solutions Fund class.

Master’s degree in business and climate solutions

Haas and Berkeley’s Rausser College of Natural Resources recently launched the concurrent MBA/Master of Climate Solutions to prepare the next generation of sustainability and climate leaders. The new program, enrolling for fall 2024, will allow students to earn a master’s degree in both business and climate solutions in five semesters, one more than is typically required for the full-time MBA.

Dean Harrison says the degree will teach critical skills and knowledge in climate data science, carbon accounting, and lifecycle analysis as well as technological and nature-based solutions. “Future business leaders will require a depth of training in both business and climate change to work across disciplines and execute competitive strategies,” she says. “This new program will provide a breadth of skill sets, equipping our grads to lead in building a sustainable, low-carbon future.”

Students in the MBA/MCS cohort will spend the first year at Haas completing MBA core coursework—which includes courses in leadership, marketing, management, finance, data analysis, ethics, and macroeconomics, along with sustainability courses—before moving to classes at Rausser. The MCS core curriculum includes climate and environmental sciences; climate economics and policies; technological, business, and nature-based solutions; training in analytical and quantitative skills; and applied exercises and engagements that emphasize adaptive thinking and problem-solving. MCS courses will translate the fundamental science and groundbreaking discoveries of UC Berkeley experts, enabling professionals to learn how to evaluate technologies, develop just climate strategies, and remove barriers to implementing practical climate solutions.

“Future business leaders will require a depth of training in both business and climate change to work across disciplines and execute competitive strategies.”

—Haas Dean Ann Harrison

Michele de Nevers, executive director of Haas’ Office of Sustainability and Climate Change, says the dual-degree’s focus on early-career professionals promises quick dividends. “These professional students are clearly positioned to make an immediate impact and will serve a critical role as translators of academic insights and enacting these insights in the world,” she says.

All MBA/MCS students will participate in a semester-long capstone program that gives them the opportunity to partner with organizations operating across the business, government, and nonprofit sectors. A unique leadership course on organizational, political, and societal change for climate solutions will prepare students to be change agents anywhere they work. Students will also complete two summer internships, which will allow for deep immersion in different disciplines and more time to build relationships.

James Sallee, a professor in the Department of Agricultural and Resource Economics and faculty director of the MCS program, says that while new research on climate solutions is still critical, many of the things needed to address the climate challenge are already known. “What we really need are people spread throughout society and the economy who are in a position to take action on climate and who are equipped with the tools to make the right choices. Educating those students is the vision of the MCS program,” he says.

New Climate Solutions Fund

Financing the climate transition requires a diverse and technical tool kit: An estimated $4 trillion to $5 trillion per year will be needed to reshape global energy, transportation, food, and waste infrastructure and to help companies reinvent supply chains and integrate new technologies, says Professor Adair Morse.

To equip future leaders with the financial know-how to accelerate the transition to a low-carbon economy, Haas is launching the student-led Climate Solutions Fund in fall 2024—the first such course at a major business school.

MBA students in the course will serve as investment managers for the $2.37 million fund, learning how to structure financing in complex private markets by investing in real-world deals focused on solutions to climate change.

It was conceived of by Morse, co-founder of the Sustainable and Impact Finance Center (SAIF). “As the world moves toward a goal of net-zero carbon emissions by 2050, we need financial leaders with the skills to navigate the economic revolution we are facing,” she says. “This economic revolution will be staggeringly disruptive yet will also be a source of more business opportunities across all parts of the country than we’ve seen in 250 years.”

The Climate Solutions Fund curriculum will teach students new designs and uses of finance not traditionally taught in mainstream finance courses, including public-private partnerships with federal and state programs, identifying the underlying technologies to fuel the low-carbon transition, and envisioning new financial products. Morse saw the need for this financial expertise while serving as deputy assistant secretary of capital access in the U.S. Department of the Treasury from 2021 to 2023.

“As the world moves toward a goal of net-zero carbon emissions by 2050, we need financial leaders with the skills to navigate the economic revolution we are facing.”

—Prof. Adair Morse

“This level of reinvestment [in the climate transition] will require every finance tool available, including designing financial structures to mobilize government programs and work with community and industry partners,” she says. “Our goal is to expand how we teach students to provide the leadership and expertise that corporations, financial entities, startups, governments, and philanthropies will need to navigate this transition.”

Students in the course will assess investment opportunities in U.S.–based for-profit companies, working with outside investment partners to structure deals. Following a pitch competition, student managers will select one finalist to co-invest $100,000 to $300,000 annually. The fund is intended to generate positive returns over time so that future students can build off the capital.

The Climate Solutions Fund was made possible by a lead gift from Allan Holt, MBA 76, along with generous founding donations from Larry Johnson, BS 72; Charlie Michaels, BS 78, and his wife, Doris; Scott Pinkus; and Professor Laura D. Tyson, former Haas dean and co-founder of SAIF.

Thomas Marschak, 93, an economist who influenced generations of students during almost 60 years of active research and teaching at Berkeley Haas, died Jan. 31 in Oakland, Calif.

Marschak was known for his generous mentorship and his research into the design of efficient organizations. “In so many ways, Tom was way ahead of his time,” said Prof. Rich Lyons. “When you think about the center of gravity of his work—the informational and incentive aspects of the design of efficient organizations—you realize quickly that these topics are becoming ever more important.” As a member of the Economic Analysis & Policy Group and the Operations & IT Management groups at Haas, Marschak made his mark in economics theory, studying information gathering, information technology, and network mechanisms. Read his full obituary.

IN MEMORIAM

Robert Kelleher, BS 51 Jay MacMahon, BS 52 William Mais, BS 54 Robert Brooke, BS 60 Donald Dauterman, MBA 62 Gary Mariani, MBA 68 Michele McLaughlin, BS 70 Justin Berglund, Friend

Luke Kreinberg, a beloved associate director and career coach of Haas’ MBA Career Management Group, passed away in El Cerrito, Calif., in February.

Articulating wisdom and experience through haiku, he seamlessly blended the serenity of the Dalai Lama with the playfulness of Cookie Monster. Luke was known for asking, “For the sake of what?” through which he advocated kindness, grace, and love, inspiring many to embrace their ‘Berkeley’ spirit. His legacy is not just in coaching but in fostering a culture of gratitude, mindfulness, and an aspiration toward one’s North Star. He will be forever in our hearts.

David Sherman, 67, an esteemed business strategist and consultant, died Jan. 28 in El Cerrito, Calif.

After Haas, Sherman became a principal at Towers Perrin and led the company’s strategy, operations, and organizational transformation. He then held leadership roles at A.T. Kearney and Blu Skye Consulting before founding Sustainable Value Partners and Cooperative Advantage.

Throughout his career, Sherman advised executives from leading global companies. Paul Rice, MBA 96, CEO of Fair Trade USA, said he’ll remember Sherman for his “brilliant mind, generous spirit, and unwavering belief in the potential of business and people to do good in the world.” Sherman served as co-president of the East Bay Chapter of the Haas Alumni Network, advisory council member of Fair Trade USA, and advisory board co-chair of Aclima Inc.

Timothy Ryan, 86, investor and philanthropist, died Feb. 12 in San Rafael, Calif. After graduation, Ryan spent two years in the U.S. Army doing counterintelligence work in Washington, D.C., before returning to Berkeley for his MBA.

Ryan went on to work for IBM as a systems engineer, then for San Francisco-based investment firm Dodge & Cox, where he became partner and worked for 36 years until his retirement.

He and his wife, Annette, were driven by improving the lives of young people and preserving the environment. Their philanthropy extended to many community organizations, including Berkeley Haas and the UC Berkeley Library Board. Ryan was also named a Builder of Berkeley. Read his full obituary.

Peter O. Shea, 88, a heavyweight in construction and real estate development, died Oct. 23, 2023, in Newport Beach, Calif., after battling Parkinson’s disease.

After graduating from Haas, Shea joined his brother and cousin as co-owner of the J.F. Shea Co., serving as VP and later president of J.F. Shea Construction, its heavy-construction subsidiary. Under his leadership, he created one of the nation’s

largest privately-held real estate developments, Shea Homes and Shea Properties.

A stalwart benefactor of Haas and Berkeley, Shea was a Haas School Board member from 1987 to 2002 and supported the opening of the Haas campus in 1994. He also served as trustee of the UC Berkeley Foundation.

Spring 2024|By Carol Ghiglieri| Photos by Michaela Vatcheva

Financial literacy class taught by Stephen Etter, BS 83, MBA 89, prepares Cal athletes for the big business of pro sports.

Layshia Clarendon, BA 13 (American studies), took Stephen Etter’s independent study and was prepared for the financial realities of turning pro before being drafted into the WNBA. They now play for the Los Angeles Sparks. Credit: Bruce Bennett/Getty Images

Shortly before Layshia Clarendon, BA 13 (American studies), was drafted into the Women’s National Basketball Association (WNBA), the Cal senior attended a pre-draft orientation. Clarendon raised a hand and inquired about matching 401(k)s. The people fielding questions were floored. They weren’t used to college students knowing what a 401(k) was, let alone being savvy enough to ask about matching contributions.

“I remember going to that meeting and thinking, ‘Oh, wow, I already know some of this,’” Clarendon recalls. When it came to financial literacy, Clarendon was miles ahead of most of their peers—all thanks to an independent study course they’d taken with Haas professional faculty member Stephen Etter, BS 83, MBA 89, called Financial & Business Literacy for the Professional Athlete.

For more than 20 years, Etter has helped scores of UC Berkeley athletes prepare for the financial realities of turning pro. Everyone from football great Marshawn Lynch and quarterback Jared Goff to Olympic swimmer Missy Franklin and golf phenom Collin Morikawa, BS 19, have learned about navigating contracts, choosing advisors, investing, and more for their post-Berkeley lives.

Now, all of these issues are relevant for students too. In 2019, legislation was passed—first in California then later throughout the National Collegiate Athletic Association (NCAA)—allowing college athletes to earn compensation for the use of their name, image, and likeness (NIL) via sponsorships. No longer are questions about agents, contracts, budgeting, and taxes part of a hypothetical future; student-athletes are facing them today, intensifying the need for Etter’s class.

“I’m working with students who are putting a half to three-quarters of a million dollars in their pocket today,” Etter says. Trouble was, his independent study only reached a small number of students. This coming fall, with the help of a grant from Robinhood Money Drills, Etter is expanding his course and bringing it to many more UC Berkeley student-athletes.

It’s how much you keep

The idea for an independent study for athletes first occurred to Etter when one of his students, Nnamdi Asomugha, BA 06 (interdisciplinary studies), approached him for some advice. Asomugha was preparing to turn pro (he was ultimately a first-round draft pick by the Oakland Raiders) and was suddenly facing major decisions that would affect his economic future. Etter, one of the founding partners of Greyrock Capital Group, had been teaching corporate finance at Haas for nearly a decade by then. He favored experiential learning with real-world applications, and helping athletes navigate the complex waters of a professional career more than fit the bill.

Athletes turning pro find themselves in an unusual position, entering highly lucrative careers while having no financial training. The eye-popping mega-salaries that generate headlines are not the norm in pro sports, but starting salaries for many athletes are nevertheless substantial. Still, as former National Football League (NFL) player Justin Forsett, BA 14 (interdisciplinary studies), put it, “It’s not how much you make, it’s how much you keep.”

Forsett, who played pro football for nine years and is now an entrepreneur and motivational speaker, says taking Etter’s course gave him a real advantage. “There weren’t a lot of courses on financial literacy when I was a kid, in high school or even in college,” he says. After gaining a solid foundation with Etter, he entered the NFL with what he calls “a conservative approach.” He explains, “I wasn’t going out getting fancy new cars. I knew it was about how much I could actually keep and save and invest in the right things.”

Prepare your future self

Each year, Etter begins the class by sharing a series of sobering statistics: 78% of retired NFL players suffer financial hardship. Nearly 16% of NFL players have filed for bankruptcy. And 60% of former National Basketball Association (NBA) players are broke. These brief, cautionary tales drive home a crucial point that’s easily overlooked by young student-athletes: While the pros earn big salaries during their careers, those careers are often short and can be wildly unpredictable.

Stephen Etter, BS 83, MBA 89, teaching his financial literacy class to student-athletes. He’s even helped some, like Elijah Hicks, BA 20 (American studies), start nonprofits. Hicks’ Intercept Poverty Foundation provided emergency grants to low-income UC Berkeley students during the pandemic.

“Steve tells us the reality,” says Cam Bynum, BA 20 (American studies), who studied with Etter and just finished his third season as a safety with the Minnesota Vikings. “The average lifespan in the NFL is three years,” he says. “If you’re blessed, you’ll make it to 10 years, maybe 12. So that means you’re retiring at 32 years old, maybe 35. That’s just half your life. So then what are you going to do?” Without Etter to prompt them, many student-athletes might never give that question much thought.

Elijah Hicks, BA 20 (American studies), a safety for the Chicago Bears, says that one of the most valuable aspects of the course was that it forced him to think ahead. “I got to put myself in my future self’s shoes,” he says. “The class puts you in scenarios before you’re actually there, so now I’m more prepared and I’m not surprised by anything that pops up, like taxes.” High-earning athletes, for instance, not only have to pay taxes in their home state but in nearly every state they play in, a fact that shocked many of Hicks’s first-year teammates—but not Hicks.

“If you’re blessed, you’ll make it to 10 years, maybe 12. So that means you’re retiring at 32 years old, maybe 35. That’s just half your life. So then what are you going to do?” —Cam Bynum

Ask the right questions

Since the course’s inception, athletes from a range of sports have studied with Etter, players heading to the NFL, NBA, WNBA, and Major League Baseball along with swimmers, golfers, and water polo players. News of the class has tended to spread by word of mouth among teammates, but coaches, too, have steered students to him. “The Cal coaches have had the insight and caring attitude to make sure they prepared their athletes for the financial aspects of their careers,” Etter says.

Not all professional careers are the same, however. Swimmer and six-time Olympic medalist Ryan Murphy, BS 17, knew he wanted to swim professionally after his success at the 2016 Rio Olympics, but he didn’t know what that entailed. In Etter’s class, Murphy’s fellow students that semester were heading for the NFL, but as a swimmer, Murphy’s professional path was less straightforward. “Our earning power is completely based on marketing,” he says. So Etter tailored the learning, helping him focus on finding a marketing agent.

“He connected me with people on campus and had me sit down for meetings with them,” Murphy recalls. Etter also encouraged him to talk to older swimmers who’d turned professional. “He was kind of a master connector for me.”

Getting out and talking to people is a big part of what Etter teaches. Whether it’s picking an agent, a financial advisor, or an insurance broker, knowing the kinds of questions to ask to make decisions that are in their own best interest is a fundamental skill he wants these athletes to learn. Sometimes, those questions come back to Etter himself. He continues to serve as a mentor to his student-athletes—they all have his number and aren’t shy about texting or calling for advice.

“This is a huge opportunity for students to start building wealth at an earlier age, especially athletes who might be first-generation college students.”

—Christian Trigg, MBA 23

Changing the playing field

Similar to professionals, NIL allows college athletes to engage in sponsorships and receive cash payments and gifts. For example, student-athletes may enter contracts to appear for autograph signings, endorse products via social media, conduct camps and clinics, post personalized video greetings, and more. However, the policy precludes students from entering pay-for-play contracts with colleges and universities.

Christian Trigg, MBA 23. Photo: Thomas Mosely.

Some Cal athletes secure deals on their own or through agents, while others are paid through the California Legends Collective, a newly formed organization (not affiliated with UC Berkeley) that’s funded by donors who together create income opportunities like those mentioned above for Cal student-athletes. Advisory Board members include Lynch, Clarendon, and Murphy.

Christian Trigg, MBA 23, director of brand development for the Cal women’s basketball program, says the new NIL rules benefit players and the team as a whole. “This is a huge opportunity for students to start building wealth at an earlier age,” he says, “especially athletes who might be first-generation college students.” In his newly created position, Trigg helps team members build their brands and secure NIL sponsorships, which in turn will help attract talented recruits to Cal. As women’s basketball coach Charmin Smith notes, “Having a strong NIL presence is critical in today’s college athletics environment.”

Junior football player Jaydn Ott is benefiting from Etter’s class while still at Cal. Ott, a running back with a likely future in the NFL, has begun earning money through NIL contracts, and he’s clear-eyed about the importance of financial literacy. “I want to understand what’s going on with my money when I speak to my financial advisors, so I’m not just giving somebody my money and saying, ‘Here, do whatever,’” he says. “I’m able to sit down and talk with them and understand what’s going on.”

Just like pros, college athletes need to understand the taxes they owe, and Etter makes sure his students do. “A lot of NCAA athletes don’t understand the difference in income and taxes between being a W-2 employee and a 1099 contractor,” he says. NIL compensation is entirely 1099, which means there is no tax withholding; players must pay estimated taxes. Etter suspects that more than a few student-athletes across the country will inadvertently fail to pay sufficient taxes. But Jaydn Ott won’t be one of them. “After Jaydn got his first paycheck,” Etter says, “he put half away for taxes. And then he was worried, so he put half of the other half away for taxes, too.”

Junior football player Jaydn Ott, who has a likely future in the NFL, has benefited from Etter’s class while still at Cal—like making sure to put enough of his earnings aside for taxes.

Spreading the wealth

Etter has long wanted to empower more students with the skills he teaches. Now, thanks to the grant from Robinhood, he’s going to. Starting this fall, the course will be reclassified as a full-fledged class rather than an independent study, which will allow more student-athletes to take it. The structure of the course is being retrofitted to accommodate up to 250 students, while maintaining the active learning style that’s a hallmark of the class. Etter will be assisted by MBA graduate student instructors who are reflective of the diverse student-athlete population.

Mary Elizabeth Taylor, vice president of international government and external affairs for Robinhood Markets, Inc., says that one of the company’s top priorities is providing the next generation with access to financial education. “Through the Robinhood Money Drills program, we are proud to give college students and student-athletes a strong foundation to responsibly manage their finances for the future,” she says. UC Berkeley is one of eight schools nationwide benefiting from the initiative.

The money is helping Etter fulfill a long-held goal. “My dream,” he says, “was to get this grant and to educate all 1,000 student-athletes at Cal.” From there, he says he’d like to bring the class to all NCAA athletes and ultimately to all 45,000 students at Berkeley.

Tastes and smells tell the stories of a place and people like nothing else. It’s an ethos that drove Aashi Vel and Stephanie Lawrence, both MBA 13, to form Traveling Spoon, a San Francisco-based food tourism business in which home cooks in 65 countries host travelers for authentic meals and cooking classes. Traveling Spoon also organizes local market tours. It’s about, as they say, “traveling off the eaten path.” Their mission is to create meaningful travel experiences, preserve culinary traditions, and provide income for locals. Here’s a look at their success.

2007

In China, Lawrence is disheartened by a “fairly touristy” dining experience. She moves to Beijing for six months, futilely searching for a Chinese grandmother who will teach her to make dumplings. Vel, in 2011, has similarly ungratifying food experiences in Mexico.

2011

During Haas orientation in August, Lawrence and Vel meet over pork tacos and bond over a shared passion for food and travel. They launch a pilot version of Traveling Spoon in December, booking customers for food explorations in India in January 2012.

Aashi Vel and Stephanie Lawrence, both MBA 13. Photo: courtesy Traveling Spoon.

2013

Traveling Spoon connects travelers with home cooks in Asia at first. Business Insider calls it one of “6 Silicon Valley startups launched in the last six months that could be huge.”

2014

The business receives $870,000 in funding, including from angel investor Erik Blachford, former CEO of online travel agency Expedia. Berkeley culinary doyenne Alice Waters is an advisor. Forbes dubs Traveling Spoon the Next Generation of Culinary Tourism.

2015

Traveling Spoon builds and automates an online marketplace and launches food experiences in 20 countries including Japan, Thailand, and Turkey.

2018

The company raises another round of funding with follow-on investment by lead investor Erik Blachford. Traveling Spoon also expands globally and scales host supply and traveler demand.

2020

Grounded by COVID, Traveling Spoon goes online, allowing armchair travelers to learn how to make dishes like noodle soup and injera from home cooks in exotic locales like Mongolia and Ethiopia. The virtual classes continue today.

2022

The business, which Forbes calls “the Airbnb for foodies,” expands to 65 countries, from Albania to Vietnam.