When the financial fallout from the pandemic hit home for her last March, Meghan Fernandes was terrified. The 29-year-old mother of three lost both her jobs—first, her position as general manager of an ice-skating rink near her home in Little Falls, New Jersey, then her part-time gig as a furniture sales rep—which cut her family's income by a third. They've stayed afloat managing on husband Mike's salary from his job at an international shipping company, plus unemployment benefits, while doing everything they can to save money. Fernandes has set up tight budgets, taken scissors to her credit cards, stopped ordering takeout, slashed spending at Starbucks and Dunkin' Donuts by 75 percent and mastered the art of home haircuts for stepson Zack, 15, and sons Colton, 5, and Hunter, 2.

It's been a traumatic six months, Fernandes says, but not all of the impact has been bad. As a result of her newfound frugality, she was able to pay off her student loan in August and expects to pay off her new car in 24 months and their mortgage in 10 years—a full decade ahead of schedule. "I've totally changed my outlook toward money," she says. Perhaps the biggest difference: a greater confidence in her ability to handle whatever comes her way. Before the virus, her family felt vulnerable to economic forces outside of their control. "Now, if something big happens again, I'll be ready," Fernandes says. "I know I won't get stressed out."

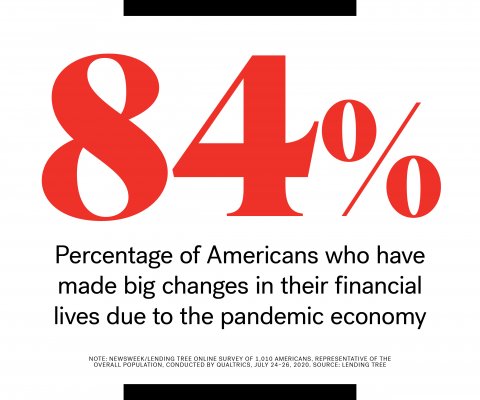

Like the Fernandes family, the vast majority of Americans have been pushed by the pandemic economy to make sweeping changes in how they manage their money—some 84 percent of Americans, in fact, according to a new nationally representative survey from Newsweek and LendingTree. As with Fernandes, many of the new habits are positive ones and nine out of 10 people expect to stick with at least some of them long after the current crisis has passed. The changes extend not just to what people do with their money but also how they feel about their financial futures and the country's—feelings that cut across age, income, gender and racial lines and are true for people whose finances have been directly affected by the pandemic as well as those who haven't taken a personal hit.

"There is a universality to this crisis," says Tendayi Kapfidze, LendingTree's chief economist. "Even though the impact is hitting people with lower incomes to a greater extent than those with higher incomes, people with more wealth feel the risk as acutely."

It's not just the layoffs and furloughs that have millions reeling, but also the pay cuts, reduced hours and fewer freelance gigs. The end of federal aid such as stimulus checks and the full $600 weekly jobless benefit, plus the loss of health insurance for some workers who have lost jobs, is hitting families hard, triggering a downward spiral. For every household that is saving more and paying down debt, there are many others that are burning through emergency savings, starting GoFundMe campaigns to help pay the rent, leaning on family and friends for aid and falling deeper into debt.

Regardless of how well or poorly you've weathered the COVID-19 economic storm, though, everyone feels the windows rattling. Only 8 percent of respondents in the Newsweek/LendingTree survey said they weren't worried at all about their family's long-term economic security in the wake of the pandemic and one in five were outright "terrified."

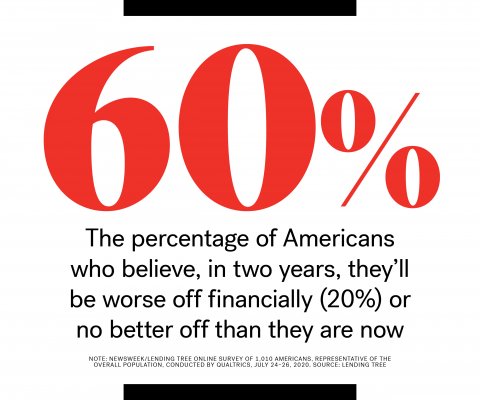

Call it PPSD, or post-pandemic stress disorder, a condition that's developing in many Americans, even though technically we're not in the "post" part of the COVID-19 crisis yet. Uncertainty about what it will take to get there, personally and as a country, is part of the problem. Some 60 percent of survey respondents expect that two years from now, they'll either be worse off financially or no better off than they are now. Says Kapfidze of LendingTree, "There is a growing resignation that it will be a long slog."

That suggests the impact of the current crisis on the way we manage money could be fundamental rather than fleeting, just as the Great Depression created a generation of compulsive savers and the 2008 financial crisis scarred our psyche for more than a decade. "When you live through a financial trauma, you actually get rewired and that experience is triggered even after it's no longer applicable," says Ulrike Malmendier, a professor of behavioral economics at the University of California, Berkeley. "If you live through a deep recession or a stock market drop, you act for several decades like you think it will happen again at any moment."

How We're Coping Now

One thing is clear from the Newsweek/LendingTree survey: People are not letting a pandemic-induced drop in their expenses go to waste—lower ( if any) commuting costs; no sporting events, concerts or movies to attend; less need for new clothes; fewer restaurant meals and takeout; minimal salon hair cuts, mani-pedis or trips to the gym or mall. Instead, those who can are saving money and adopting frugality with a vengeance.

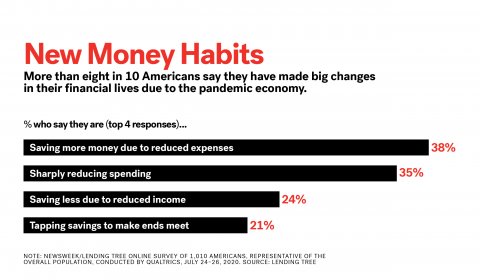

The most common changes in financial behavior: saving more money, cited by 38 percent of respondents (including roughly half of those who have been laid off or furloughed), and sharply reducing spending, named by 35 percent (1,010 Americans were surveyed from July 24–26). In fact, according to the Bureau of Economic Analysis, the nation's personal savings has been going off the charts since spring, shooting up from 8.3 percent in February just before lockdowns began to a stunning 33.5 percent in April before dropping down to 17.8 percent in July—still more than double the pre-pandemic rate. And respondents expect they'll continue to build up their emergency funds and practice frugality even after the economy regains some semblance of normalcy.

But the survey also revealed more painful changes many Americans have had to make in their financial lives. To make ends meet, one in five respondents are drawing down their savings and nearly a third have had to take on debt or to rely on financial help from family and friends to get by. Communities of color are struggling the most, with 21 percent of Black respondents saying they have had to rely on family and friends for help compared to 15 percent of white and 18 percent of Hispanic respondents.

It's a situation that seems destined to get worse before it gets better as rising infection rates slow down or postpone the reopening of schools and businesses and a new round of federal help is stalled in Congress. Adding to the challenges Americans face: Many of the forbearance and delayed-payment plans that companies and creditors extended to consumers at the beginning of the pandemic are coming to an end. Says Billy Hensley, president and CEO of the National Endowment for Financial Education, "It's creating a new level of stress many weren't facing a few months ago."

Men and women seem to be responding differently to the pressures of pandemic money management, perhaps because their experiences have been so different. Women have suffered a disproportionate share of job losses since the crisis began, according to data from the Bureau of Labor Statistics, and those who have continued to work are more likely to be essential workers who are more vulnerable to catching the virus.

It's not surprising, then, that only about one-quarter of women have been able to save more money since the pandemic began vs. roughly half of men, according to the Newsweek/LendingTree survey. The amounts men have been able to save are higher too: $511 a month on average, vs. just $253 for women. Men were also more likely to say they'll continue their higher levels of saving once the pandemic is over; women, meanwhile, were more apt to say the habit they'll keep up is their embrace of frugality.

Women are also feeling more pessimistic about their financial futures. Only three in 10 women believe they'll be better off financially two years from now, compared with just over half of the men.

What Me, Worry?

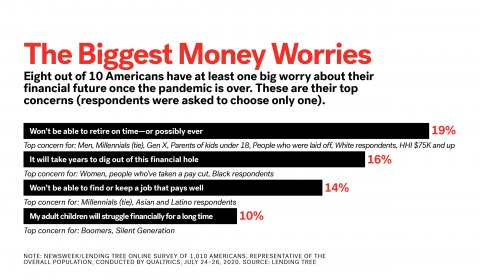

Adding to the financial anxiety that all people are feeling these days: the suddenness of this economic earthquake and the uncertainty about when it will end. In the Newsweek/LendingTree survey, fully 45 percent of respondents said they were "terrified" or "pretty worried" about their family's long-term financial security. Parents of children under 18, Gen Xers and people who had been laid off expressed the highest levels of concern.

What are we most worried about? Fear of being unable to retire on time "or possibly ever" topped the list, and was of greatest concern to the largest number of demographic groups, including men, Gen Xers, people who have been laid off, white respondents and more affluent households earning $75,000 a year or more. Meanwhile, Generation Z, women, people who've taken a pay cut and Black respondents were most concerned with how long it will take them to dig out of their current financial hole. Boomers were most worried that their adult children will struggle financially for a long time and their millennial kids were stressed about that, too—concerns about being unable to find or keep a well-paying job topped the list for millennials, as well as for Asian and Latino respondents.

Those fears are well-founded. A July report for Brookings by a trio of economists estimated that a third or more of the jobs lost from March to mid-May will not come back. "We are transitioning into a second phase where a lot of temporary layoffs are now permanent layoffs," says Kapfidze. "People who expected to return to a job are now realizing that job won't be there to return to."

Yet tough times can also bring about a reordering of priorities and positive changes. In the Newsweek/LendingTree survey, people reported being less materialistic (31 percent) these days. We are also spending more time with family and friends (32 percent) and giving back to our communities (19 percent).

"People are more conscientious with their dollars," says Lynnette Khalfani-Cox, a personal finance expert and author, known as The Money Coach. "They're saying they want to spend more locally or with communities of color or from a social justice perspective. Some people are saying 'I want to donate more to my local hospital or clinics or to health care workers in general.' That's a big shift."

Sticking With the Program

Will these changes last beyond the immediate economic crisis? History suggests that the end of the pandemic is not likely to quickly heal the national trauma that resulted from it or wipe out the new financial habits Americans are developing. It's not just the lifelong penny pinchers that emerged from the Great Depression. Many people who lived through the market crash of 2008 shied away from putting money in stocks, even when equities were booming again. The lesson: Modern survivors of economic calamities are likely to behave in ways not always justified by the objective reality in front of them.

In her studies, Berkeley professor Malmendier and her colleagues found that young people's experience in the stock market had a tremendous influence on them decades later, regardless of whether that experience was positive or negative. The researchers found that people who received low returns in the 1970s shied away from the market for years afterward. Conversely, after experiencing high returns in the 1990s, people continued to invest heavily, regardless of market conditions.

Spending habits followed the same pattern. The study authors discovered that people who lived through a period of economic shock and high unemployment later spent significantly less on food and consumer goods than their income, wealth and a lower unemployment rate would seem to indicate.

The aftershocks of today's upheaval are likely to be just as powerful. "If we have a vaccine by the end of the year, and people get their jobs back, and March 2021 looks just like March 2020 but without the crisis, pretty much all the standard models would say that people will act as if there had never been a crisis," Malmendier says. "And I'm saying absolutely not. For years, if not decades to come, you will assign some probability of this occurring again. On the bright side, you will be a more cautious spender and probably accumulate more wealth in the long run because you'll be saving a lot of money."

Certainly, if the people who say they'll continue to save more for emergencies after the economy recovers follow through, they'll be a lot better off. Various studies have shown that Americans are woefully short on cash to see them through the proverbial rainy day, let alone the recent barrage of financial hurricanes. The Federal Reserve has found, for example, that four in 10 adults could not pay a surprise $400 expense without running a balance on their credit card or turning to family and friends for help. Even people who had ample savings before the downturn may have burned through their stash: A recent survey from Bankrate found only 16 percent of Americans are currently "very comfortable" with the amount of their emergency savings.

That, in turn, can have a ripple effect on retirement plans. A survey by the Secure Retirement Institute found that workers who had to wipe out their emergency funds because they lost their jobs or saw their incomes cut because of the pandemic were twice as likely to tap into their retirement savings as those who kept their jobs.

By contrast, people who have been able to leave their retirement dollars in the stock market have benefited from its stunning resilience, with the S&P 500 index reaching a record high in August, after a calamitous drop early in the pandemic. "We're pleasantly surprised that we're not seeing a large percentage of our customers withdrawing all their money and going into cash," says Nick Holeman, a financial planner at Betterment, an online investment firm. "For the most part, wisely, they are staying the course."

"Economic Scarring"

Powerful experiences have such a lasting impact on our behavior, neuroscientists say, because such moments fundamentally alter the hardware of our brains. A process called "emotional tagging" tells our brain that an experience is important and should be remembered. The more intense the emotion, the stronger the neurological signals. These experiences—whether positive or negative—become seared in our memory and have a far greater impact on our decision-making than whatever facts and figures we might be exposed to. The result is financial decisions that may feel right but are not always terribly rational.

That helps explain why millennials became so thrifty after the financial crisis of 2008, even after the economy recovered. Studies show these younger workers were less likely to use a credit card, paid off debt sooner and carried a lower balance than their older counterparts. In 2010, more young households had no credit card debt than was true in 2001, according to the Pew Research Center. Millennials were also more conservative with their investments. A Harris Poll conducted for the Transamerica Center for Retirement Studies found that 20 percent of that age group kept their money in low-risk investments like bonds and money market funds compared to 15 percent for older generations and were more likely to say the market is scary or intimidating. The same study showed that nearly 40 percent of millennials are considered "super savers," defined as people who save more than 10 percent of their income.

As powerful as the psychological and emotional effects of major macroeconomic events are, the pandemic of 2020 is shaping up to have a lasting impact in other ways as well. The massive job losses of the past five months, for example, are likely to have an enormous long-term impact on people's earnings. Prolonged joblessness often means accepting a pay cut to get back to work, especially when entering a new field, or settling for freelance or part-time employment. Displaced workers lose 20 percent of their cumulative lifetime earnings and the impact on wages can last a full 20 years, according to research from the University of California, Los Angeles. The damage is much worse during recessionary times, researchers found, with long-term earnings losses two to four times larger than during an economic expansion.

"Your whole career can end up being impacted by the chance timing of when you happen to lose your job," says Jennie Brand, a professor of sociology and statistics at the University of California, Los Angeles.

With the job market so unpredictable, there has been evidence that more workers are going freelance or starting their own businesses. For instance, people applying for Employer Identification Numbers, which new businesses file with the IRS, are rising quickly, beyond the rate seen during the Great Recession. Financial planner Kevin Mahoney expects this shift will be permanent for many: "People who never gave entrepreneurship a thought will try to take more control of their income because of the pandemic so that in future crises, they aren't at the mercy of an employer."

Perhaps the biggest losers in today's crisis are millennials, many of whom are still reeling from the financial crisis of 2007–2008. Studies show that graduating into a recession can reduce annual earnings by 9 percent initially, as workers tend to start at smaller and lower-paying firms, and the losses do not abate until 10 years later. Which means that just as the playing field began to level for people who entered the workforce a decade ago, the pandemic recession has knocked them on their heels again. Also likely to be feeling pretty traumatized these days: the Gen Z class of 2020, who have the very bad luck to be graduating into the worst job market since the Great Depression and are totally rewriting the script for their entry into adulthood.

While recessions are often thought of as short-term events, research suggests that what experts call "economic scarring" can last for decades. A report by John Irons of the Economic Policy Institute lays out the consequences: Lower incomes for families can mean lack of educational opportunities for their children. Steep declines in spending keep new businesses from being launched and cause bigger firms to cut back on research and development that could lead to new products, spin-off companies and more jobs. The psychological and emotional toll also does not vanish when the economy recovers. People who experienced setbacks in their finances, jobs or housing during the Great Recession were more likely to be depressed, anxious and abuse drugs. Worse, such mental health issues were still evident for years after the recession ended.

Glass Half Full

Yet, despite the seemingly endless cascade of bad news about the virus and the economy, many Americans remain optimistic about the financial future. In the Newsweek/LendingTree survey, there were, after all, 40 percent of respondents who expected to be in a much better place financially within two years. And nine in 10 thought there was an upside to the crisis that will last as people adopt healthier money habits and values.

And while the pandemic and economic fallout has led many to become jaded about the prospects for getting ahead in this country, a sizable minority are still believers in the American Dream. In fact, the survey found that 17 percent of respondents have actually become more optimistic about the chances of getting ahead in America as a result of their pandemic experiences.

That may be because the complex brain process of emotional tagging does not only apply to traumatic events like recessions and massive layoffs, but also to affirmative experiences with money. At a time when some workers are using credit cards less, saving more and seeing their bank accounts swell, many young adults are seeing the crisis as a chance to get their financial act together. In a recent survey by Northwestern Mutual, nearly one fifth of millennials and one-quarter of Gen Z respondents did not have a financial plan before the pandemic but are developing one now.

Meghan Fernandes is one of them. The process of taking a deep look at what her family was doing wrong financially and taking concrete action to remedy it has been transformative, she says. "I felt very dark, very depressed, when the pandemic hit," says Fernandes, who expects to return to her job at the skating rink in September. "Now I feel like we're in a much better place."

Note: The Newsweek/LendingTree survey was an online survey of 1,010 Americans, representative of the overall population, conducted July 24–26, 2020 by Qualtrics.

Paul Keegan is a freelance writer and co-author, with City Winery founder Michael Dorf, of Indulge Your Senses: Scaling Intimacy in a Digital World. He has also written for The New York Times Magazine, Esquire, GQ, Fortune, Inc. and Outside.